A Director’s Loan Account (DLA) records money a director takes from or lends to their company outside of salary, dividends, or expense reimbursements.

A Director’s Loan Account becomes overdrawn when the director takes more money from the company than they are entitled to. In effect, the director has taken a loan from the company.

This guide explains:

What an overdrawn Director’s Loan Account is

How it happens

How to repay it

The tax implications and Section 455 tax rules

How to prevent it happening again

What Is an Overdrawn Director’s Loan Account?

A Director’s Loan Account becomes overdrawn when a director withdraws more money from the company than:

Salary received

Dividends declared

Money previously loaned to the company

When this happens, the director effectively owes money back to the company.

This is treated as a loan from the company to the director.

How a Director’s Loan Account Becomes Overdrawn

Directors typically take money from a company in three ways:

1. Repayment of money they previously lent the company

If a director puts their own money into the business, the company can repay it tax-free.

2. Salary through payroll

Directors usually take a tax-efficient salary through PAYE.

3. Dividends from company profits

Dividends can only be paid from after-tax profits.

If a director withdraws more money than these three sources allow, the Director’s Loan Account becomes overdrawn.

Example of an Overdrawn Director’s Loan Account

Tom owns a limited company.

During the year:

Tom lent the company £2,000

Tom received £9,600 salary

His accountant confirms £25,000 available dividends

Total Tom can withdraw:

£2,000 loan repayment

£9,600 salary

£25,000 dividends

Total: £36,600

However, Tom has already withdrawn £48,000 from the business.

This means Tom has taken £11,400 more than he is entitled to.

Tom’s Director’s Loan Account is therefore overdrawn by £11,400.

Tom now owes the company £11,400.

How to Clear an Overdrawn Director’s Loan Account

There are several ways to repay an overdrawn Director’s Loan Account.

1. Repay the Money Personally

The simplest solution is to transfer the money back to the company from your personal bank account.

This clears the loan immediately.

2. Declare Dividends

If the company has sufficient profits, dividends can be declared and used to offset the loan balance.

Example:

Loan owed: £11,400

Dividend declared: £11,400

The loan account becomes zero.

3. Increase Salary or Pay a Bonus

A director can take additional salary or a bonus through payroll and use this to repay the loan.

However, this will trigger:

PAYE income tax

National Insurance

So professional advice is recommended.

4. Leave It Until Future Profits

The company can declare dividends in the following year and apply them to the outstanding loan.

However, this must be done carefully because tax deadlines apply.

5. Write Off the Loan

In some cases the company may write off the loan.

If this happens:

It may be treated as dividend income

Income tax may be payable by the director

Section 455 Tax on Overdrawn Director’s Loan Accounts

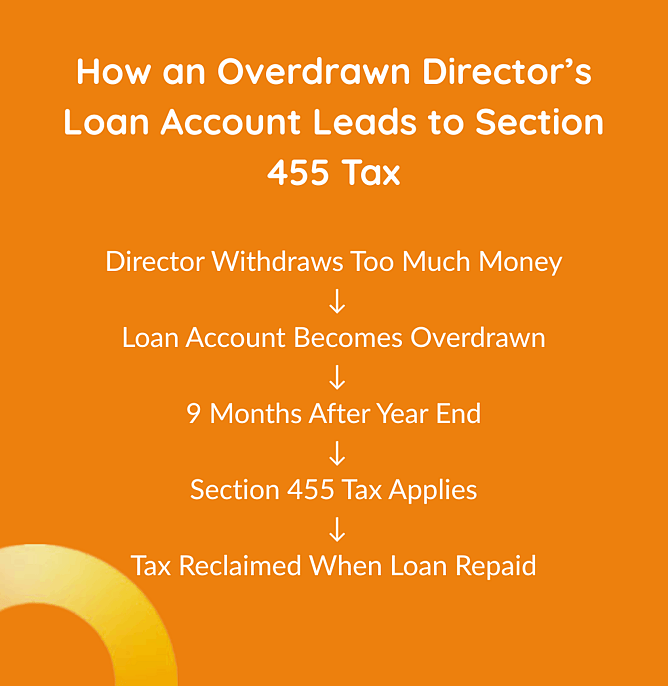

If the Director’s Loan Account remains overdrawn 9 months and 1 day after the accounting period ends, the company must pay Section 455 tax.

The tax rate is currently 33.75% of the outstanding loan.

Example:

Loan balance: £11,400

Section 455 tax:

£11,400 × 33.75% = £3,847.50

This tax is paid through the company’s corporation tax return.

Can Section 455 Tax Be Reclaimed?

Yes.

If the director repays the loan later, the company can reclaim the Section 455 tax from HMRC.

However, the reclaim usually happens after the end of the accounting period when the loan is repaid, meaning the company may wait some time to recover the tax.

Flowchart showing how an overdrawn Director’s Loan Account can trigger Section 455 tax if not repaid within 9 months after the year end.

Benefit in Kind Tax on Director’s Loans

If a Director’s Loan exceeds £10,000 at any point in the year, HMRC may treat it as a benefit in kind if no interest is charged.

This means:

The director pays income tax on the benefit

The company pays Class 1A National Insurance

The benefit is calculated using HMRC’s official interest rate.

Example:

Loan balance: £11,400

HMRC official rate: 2.25%

Interest benefit:

£11,400 × 2.25% = £256.50

This amount is declared on the director’s P11D form.

How to Reclaim Corporation Tax Paid on Director’s Loans

If Section 455 tax has been paid, the company can reclaim it once the loan is repaid.

This can be done:

Within the next corporation tax return, or

By submitting Form L2P to HMRC

The reclaim must usually be made within 4 years of the loan repayment.

How to Prevent an Overdrawn Director’s Loan Account

The best way to avoid problems with Director’s Loan Accounts is good financial management.

Key steps include:

Keep bookkeeping up to date

Regular bookkeeping allows you to see how much you can safely withdraw.

Use management accounts

Monthly or quarterly management accounts show:

Company profits

Available dividends

Loan balances

Plan withdrawals with your accountant

Your accountant can help structure income through:

Salary

Dividends

Pension contributions

This ensures withdrawals remain tax-efficient and compliant.

Summary

An overdrawn Director’s Loan Account occurs when a director withdraws more money from the company than they are entitled to through salary, dividends, or loan repayments.

The balance can be cleared by:

Repaying the money personally

Declaring dividends

Increasing salary or bonuses

Writing off the loan

If the loan is not repaid within 9 months and 1 day after the company year end, the company must pay Section 455 tax.

Keeping accurate bookkeeping and reviewing finances regularly can help prevent Director’s Loan Accounts from becoming overdrawn.

If we can help in any way, please contact us

Common FAQs

Can a Director’s Loan Account be written off?

Yes. The company can write off the loan, but the amount may be treated as income or dividends for tax purposes.

What is the 9-month rule for Director’s loans?

If a loan to a director is not repaid within 9 months and 1 day of the accounting period end, the company must pay additional corporation tax.

Do directors pay interest on loans from their company?

If the loan exceeds £10,000 and no interest is charged at HMRC’s official rate, the loan may be treated as a benefit in kind.